加群或其他问题可扫二维码添加阿瑟

加群或其他问题可扫二维码添加阿瑟

Looking for Best Virtual Card? A stable virtual card for ChatGPT Plus, Claude, or Midjourney in 2026? Discover the best Virtual Visa and Mastercard platforms (DogPay, BinPay, CoinePay) with proven success rates. Solve "card declined" issues, learn about 5371 BIN segments, and compare fees for overseas subscriptions and e-commerce.

Last Updated: December 25, 2025

💡 Looking for virtual card applications or recommendations? This article summarizes the most stable virtual card platforms for 2026, covering Virtual Visa and Mastercard, to solve your overseas payment troubles.

The answer is simple—because you are constantly prompted when subscribing to GPT: “your card has been declined.”

In 2025, risk controls on various platforms worldwide have undergone multiple upgrades. Traditional dual-currency credit cards are frequently rejected when subscribing to many overseas services, such as ChatGPT, Claude 3.5, Gemini 3, or Midjourney.

It’s as if these platforms don’t want to take my money!

Actually, the common reason for rejection is platform risk control. Currently, many overseas applications are not open to users in Mainland China or even Hong Kong. Therefore, using credit cards from these regions generally won't work.

Previously, Arthur recommended many virtual card platforms, but quite a few have shut down, “run away,” or stopped services. Platforms like WildCard, Formcard (Formpay), and Dupay have all stopped services and can no longer be used.

The platforms are gone, but market demand keeps increasing—we still need cards, right?

So, in the final days of 2025, let’s summarize which virtual card platforms are still supported, their respective advantages, and their fee structures. This guide aims to provide the most reliable payment solutions for 2026 overseas consumption, AI subscriptions, and cross-border e-commerce.

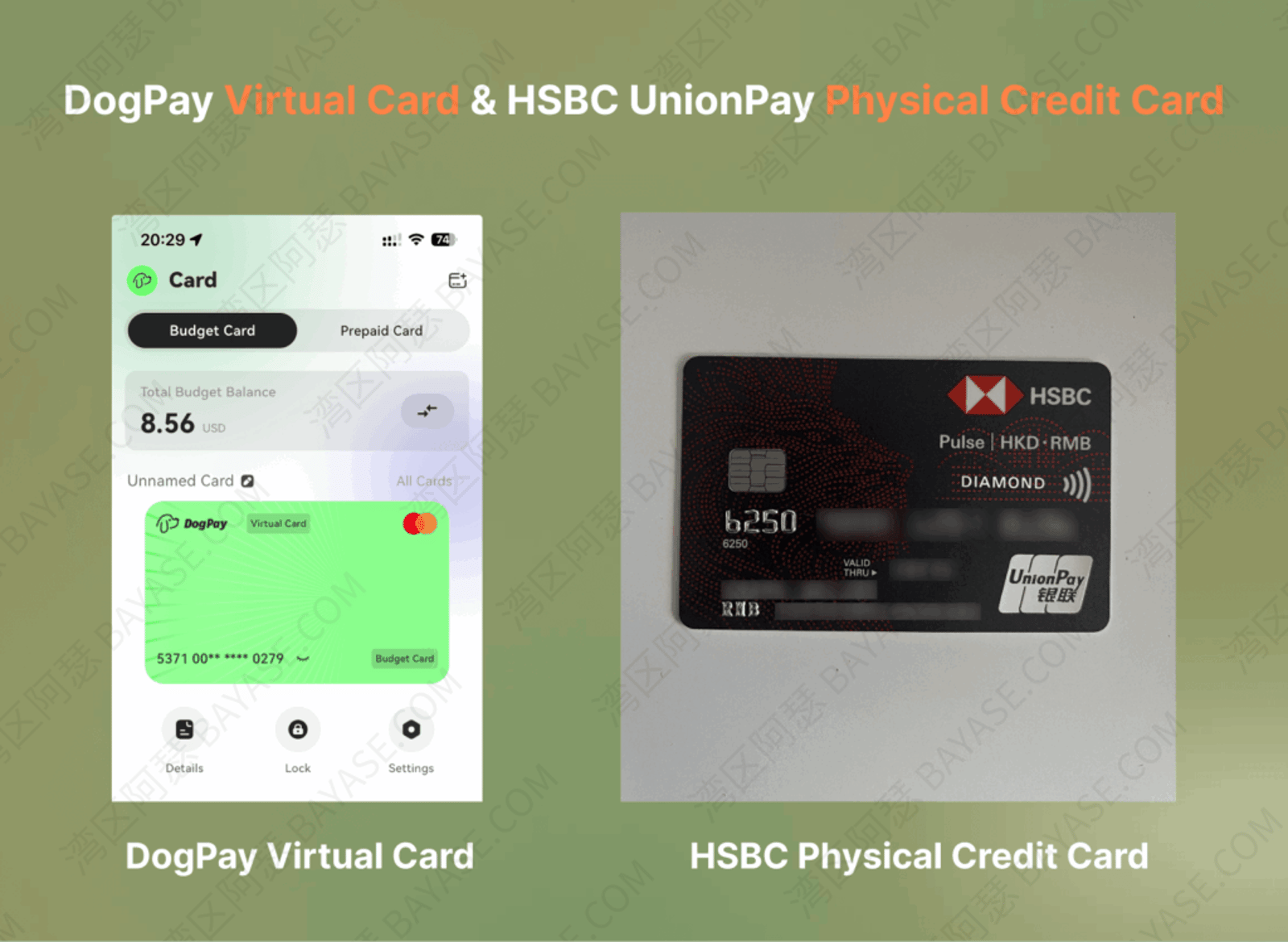

We personally tested the 5371 BIN of the DogPay platform on December 24, 2025, and successfully renewed ChatGPT. During the test, we topped up the budget card with 22 USD. After deducting the 20 USD subscription fee, the real-time billing showed a successful charge with no risk control pop-ups throughout the process.

A Virtual Card is essentially a bank card that does not exist as a physical plastic card. It usually exists in the form of Visa or Mastercard and is primarily used for online payments, subscription services, and cross-border consumption.

A standard virtual card is structurally identical to a physical bank card, typically containing the following core information:

As long as you have the above information, a virtual card can complete payments on platforms that support Visa / Mastercard, just like a physical bank card.

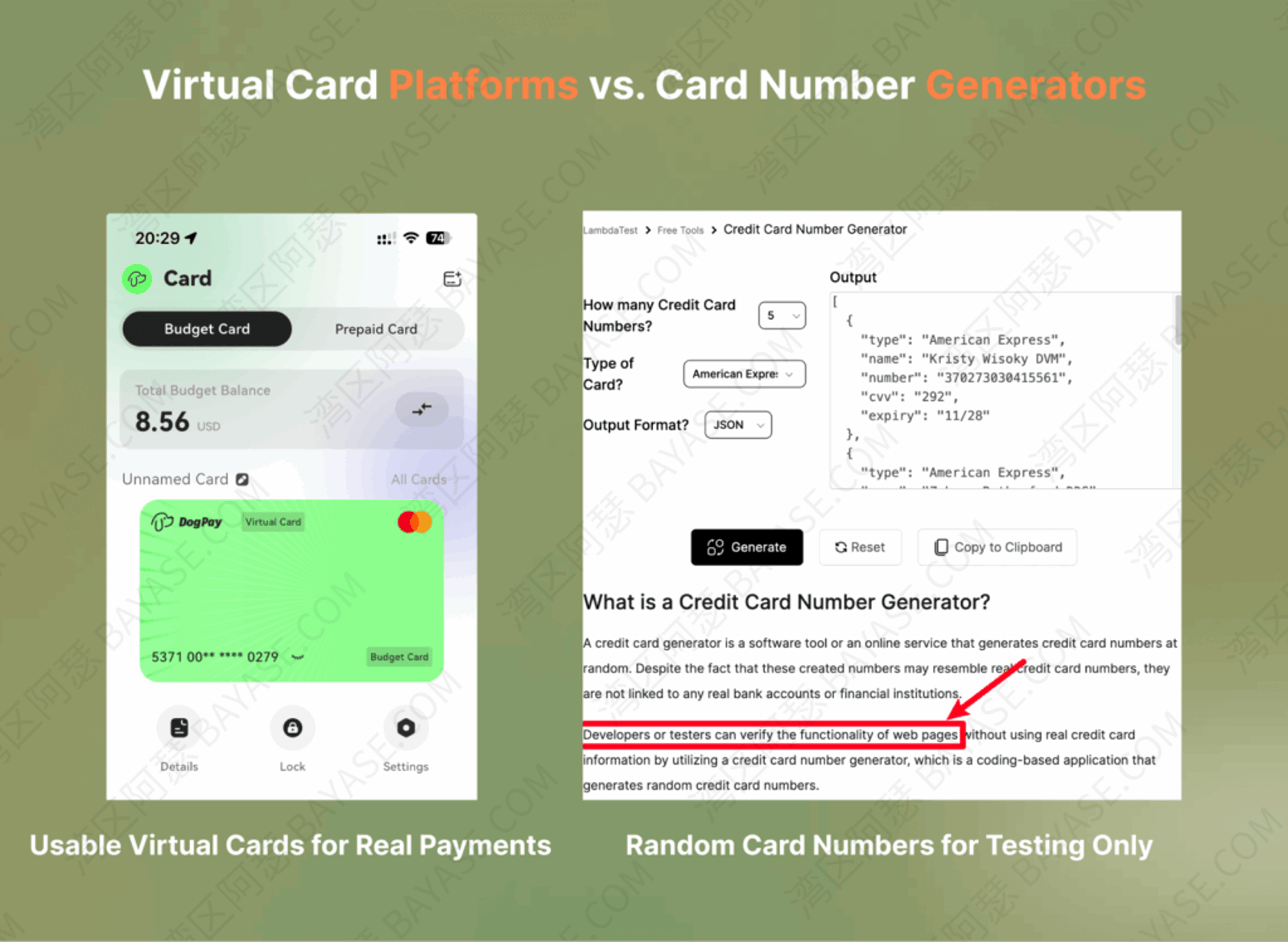

It is important to distinguish between “virtual card number generators” and “real virtual card platforms”:

Simple understanding:

Whether money can be successfully deducted is the key to distinguishing a “fake virtual card” from a “real virtual card.”

Among the many types of virtual cards, Visa / Mastercard virtual cards currently have the highest approval rates and the widest range of applications. For example, the UnionPay logo often seen on Mainland China bank cards is also the logo of a card organization (“UnionPay”), but its global application range is not yet high.

First: High approval rate and strong global universality.

Visa and Mastercard are the world's most widely covered international card organizations. Almost all mainstream overseas platforms—including e-commerce websites, SaaS tools, cloud services, and subscription products—support these two organizations by default. Compared to some regional card types or niche payment methods, Visa / Mastercard virtual cards are more mature in risk control identification and payment compatibility, making them less likely to encounter “card not supported” or “payment failed” issues in actual use.

Second: Better privacy and fund security control.

One of the core advantages of virtual cards is isolation from the primary card or main account:

For users who frequently conduct cross-border payments, try overseas services, or bind cards to unfamiliar platforms, a Visa / Mastercard virtual card acts like a “security buffer,” completing the payment while effectively controlling risk.

From a practical standpoint, this is why most compliant virtual card platforms prioritize providing Visa or Mastercard virtual cards over other niche card organizations.

In these scenarios, virtual cards often ‘show their power.'

A virtual card that can pay stably will definitely be the most popular, which is why finding the Best Virtual Card is essential for ensuring uninterrupted access to global services.

By selecting a high-tier provider, you can bypass strict payment filters and enjoy a seamless subscription experience across all your favorite AI and entertainment platforms.

Arthur has written articles introducing BinPay, DogPay, and CoinePay, but has never put them together for comparison. To help you choose the most suitable virtual card, I’ve made a detailed comparison here.

💡 Expert Tip: In 2026, choosing a card depends on “BIN stability.” The following platforms all support top-ups via Alipay/WeChat or Cryptocurrency.

The table below is the 2026 virtual card platform comparison chart organized by Arthur, covering the fees and application scenarios of mainstream platforms:

| Virtual Card Platform | Core Advantage | Recommended BIN | Suitable Scenarios | Min. Fee | Card Org | Region |

| Roogoo | 0 card issuance fee, supports Apple Pay / Google Pay, ChatGPT, Gemini 3 and others | Premium Card (card BIN assigned automatically) | AI subscriptions, beginner-friendly | 0 USD | MasterCard / Visa | US/HK |

| DogPay | Supports Apple/Google Pay, GPT/Gemini 3; Excellent App | 5371 | AI Subs, Beginners | 10 USD | Mastercard | US/UK/HK |

| CoinePay | Huge amount of BINs; Choose cards by scenario | 5177/5436/4288 | General consumption, Ads, E-commerce | 3.99 USD + 10 USD initial top-up | MC / Visa | US/HK/SG |

| WASABI Card | Huge amount of BINs; Quick view of supported merchants | 4288 | General subscriptions (cannot bind e-wallets) | 10 USD | MC / Visa | US/HK/SG |

| PokePay | Visa card; Physical card free shipping in Asia | 4413 | Overseas subscription pre-authorizations | 5 USD | Visa | US |

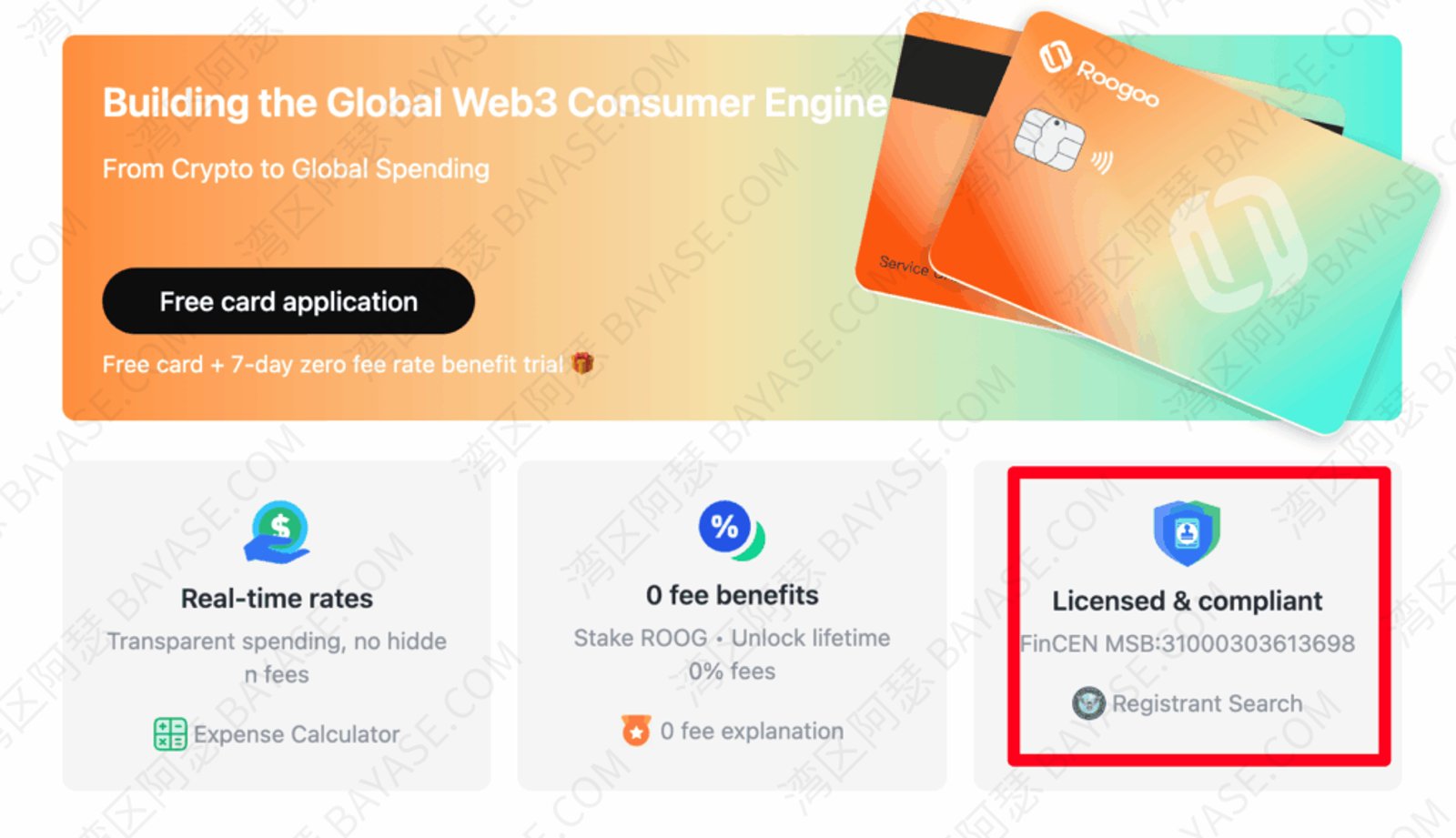

This is a card that Arthur recently started using, because recently many people found that DogPay now requires proof of an overseas address, so there is an urgent need to find a new virtual card payment solution.

Then Arthur discovered the Roogoo platform, and found that it does not require a card issuance fee. Compared with the other platforms mentioned earlier, this alone is already very good.

Of course, besides the card issuance fee, fund security is also important. Arthur wanted to check what kind of qualifications it has, and immediately saw it stated clearly on the homepage, with a verification link attached. It holds a U.S. MSB compliance license.

Roogoo is a borderless payment service platform. Roogoo cards are designed to build a global Web3 consumption engine. You can recharge with cryptocurrency and enjoy truly borderless global payments.

Roogoo provides many products for merchants and developers, allowing them to accept crypto asset payments from customers and also make payouts to customers through batch APIs. It can intelligently block forged or blacklisted crypto assets such as USDT, providing an unmatched level of convenience and security for both receiving and sending payments.

Currently, Roogoo supports both MasterCard and Visa BINs, and there are three types of cards in total: Premium Card, Boundless Card, and Joy Card. To make it easier for everyone to understand, Arthur created a table below for reference:

| – | Premier Card | Borderless Card | Enjoy Card |

| Card Schemes | MasterCard | Visa | Visa |

| Region | US Card(Puerto Rico) | Hong Kong Card | US Card |

| Card Issuance Fee | 0USD | 0USD | 0USD |

| Initial Top-up After Issuance | 10USD | 10USD | 10USD |

| Top-up Fee | – | – | – |

| Transaction Fee | 1% | 0.8% | 1% |

| Cross-border Fee (non-USD transactions) | 1.6% | – | 1.6% |

| Authorization Fee (only charged when the transaction amount is < $30) | – | $0.35/transaction | – |

| Exchange Rate | Real-time exchange rate | Real-time exchange rate | Real-time exchange rate |

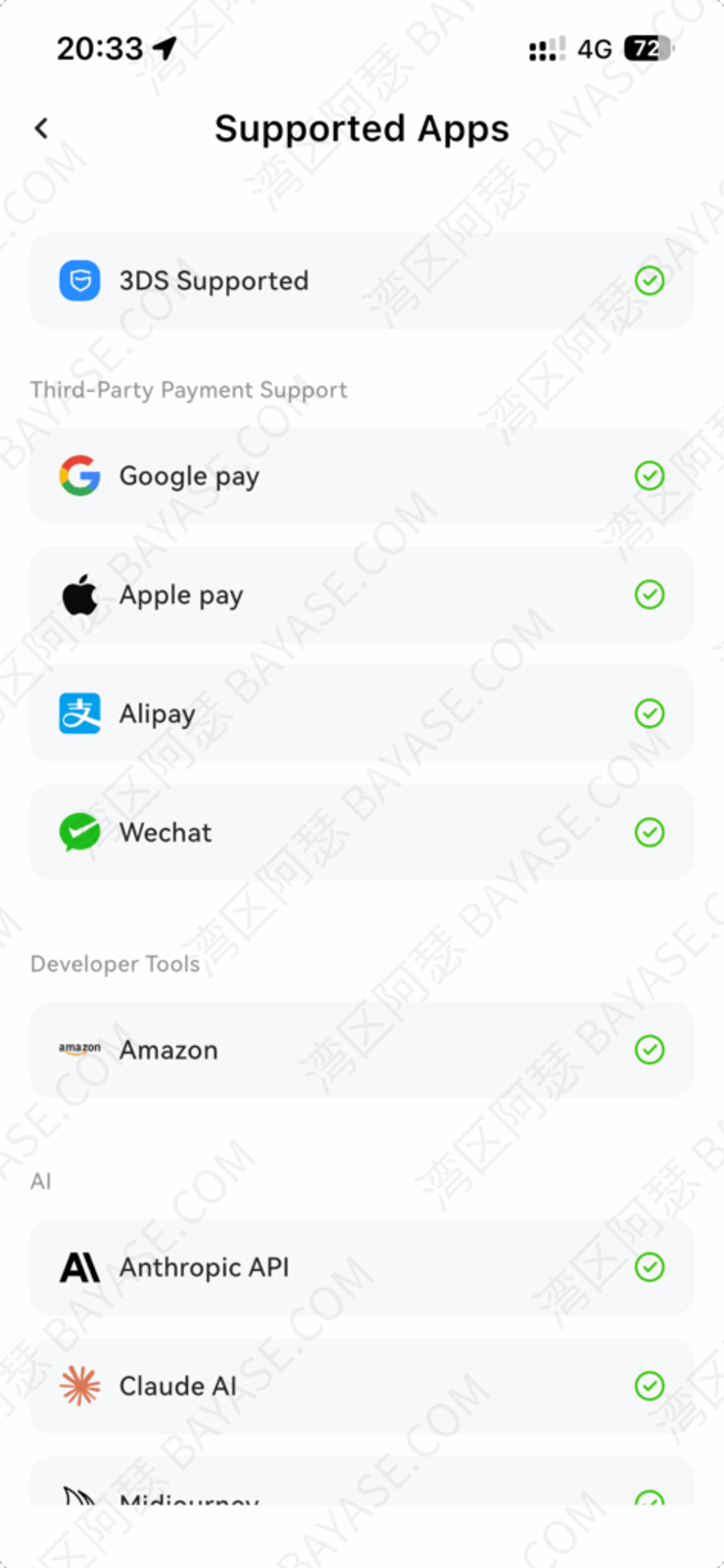

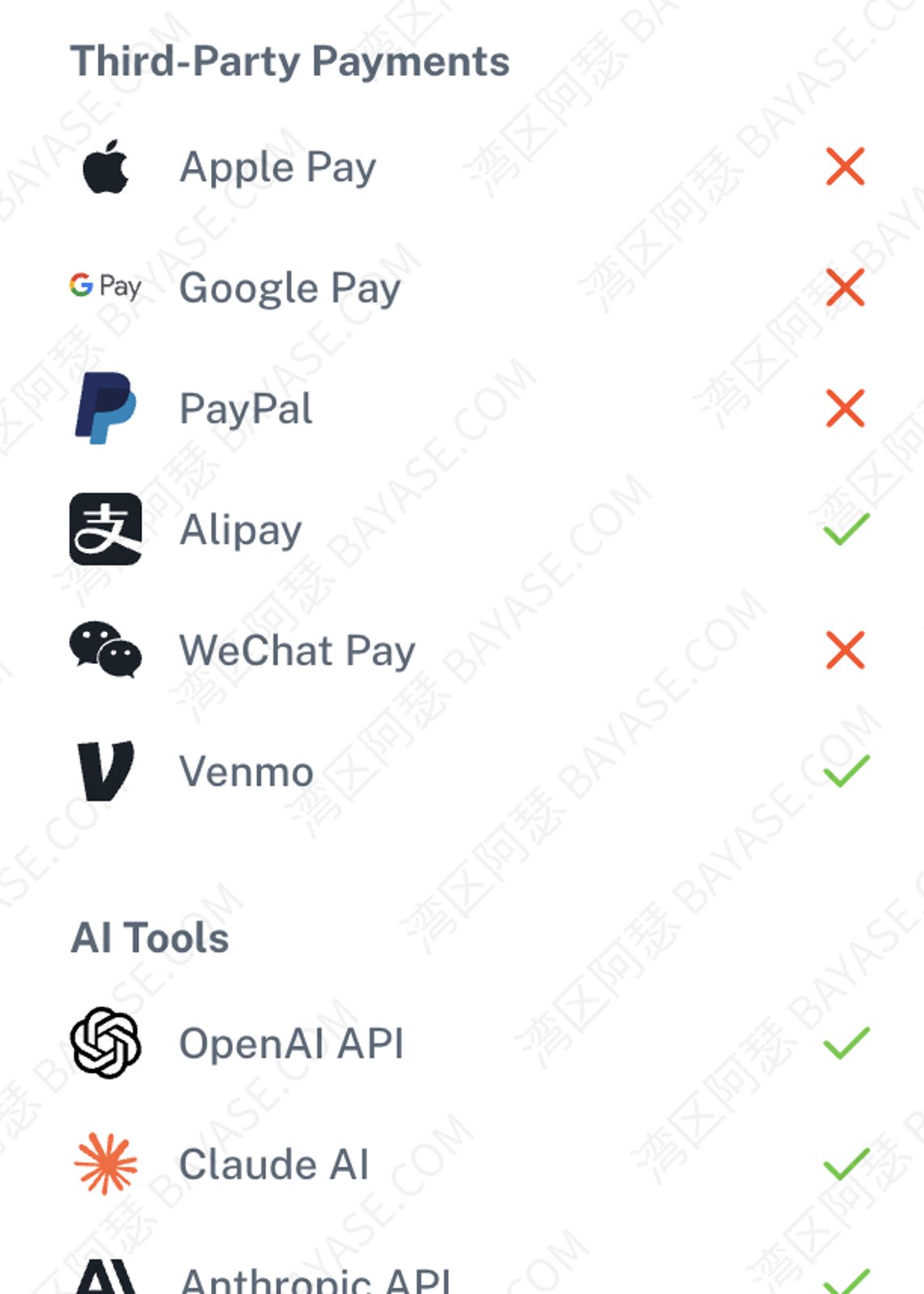

| Apple Pay / Google Pay / AliPay Support | All supported | All supported | Apple Pay not supported yet, others supported |

| AI Subscription & Payments | OpenAI API ✅ Claude AI ✅ Anthropic API ✅ Midjourney ✅ | OpenAI API ❌ Claude AI ❌ Anthropic API ❌ Midjourney ❌ | OpenAI API ✅ Claude AI ✅ Anthropic API ✅ Midjourney ✅ |

| Summary | More suitable for daily spending and AI subscription services, smoother payments | More suitable for large transactions and travel spending | More suitable for daily spending and international online/offline payments and subscriptions, smoother payments |

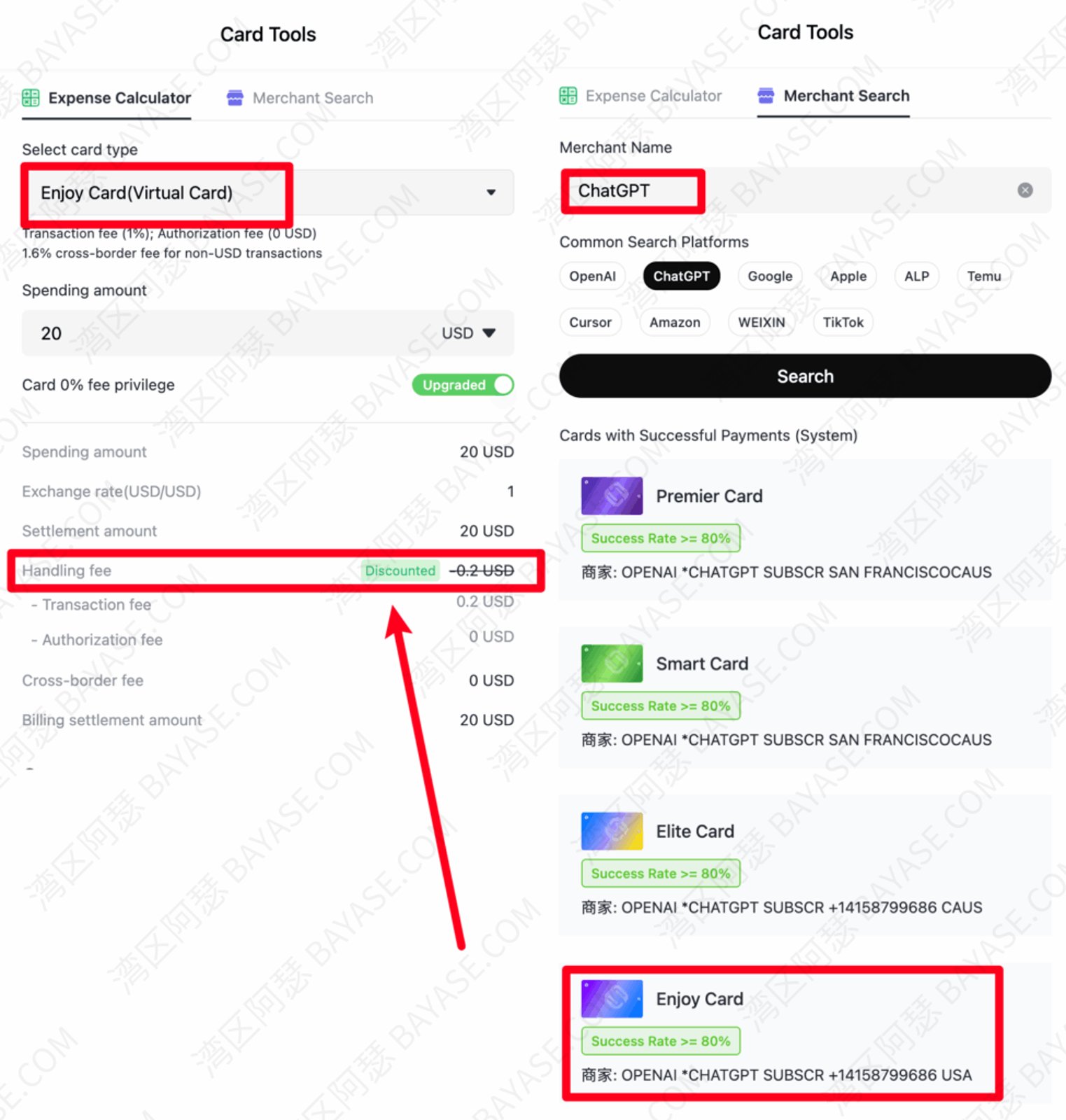

Overall, the fees actually look very reasonable. If you register through the exclusive signup channel in this article, not only is the card issuance fee waived, but the first card can also be used with a 0% fee trial within 7 days after activation (limit 200 USD).

I think it’s pretty good. At the very least, for me right now, topping up GPT works without any problem.

As for the fees, the official website also provides a fee calculator. You can directly calculate the cost and the payment success rate when applying for the card, which is actually very useful.

Roogoo is a borderless payment service platform. Fee calculator.

Arthur won’t say much more. In short, this is the best platform Arthur has used besides DogPay, and for now, there is no other one that comes close.

This is the virtual card I have been using long-term. During this period, there were indeed changes in card segments, but the platform provided new replacements. It is overall stable and reliable.

Currently, DogPay only has a virtual card business, divided into two types:

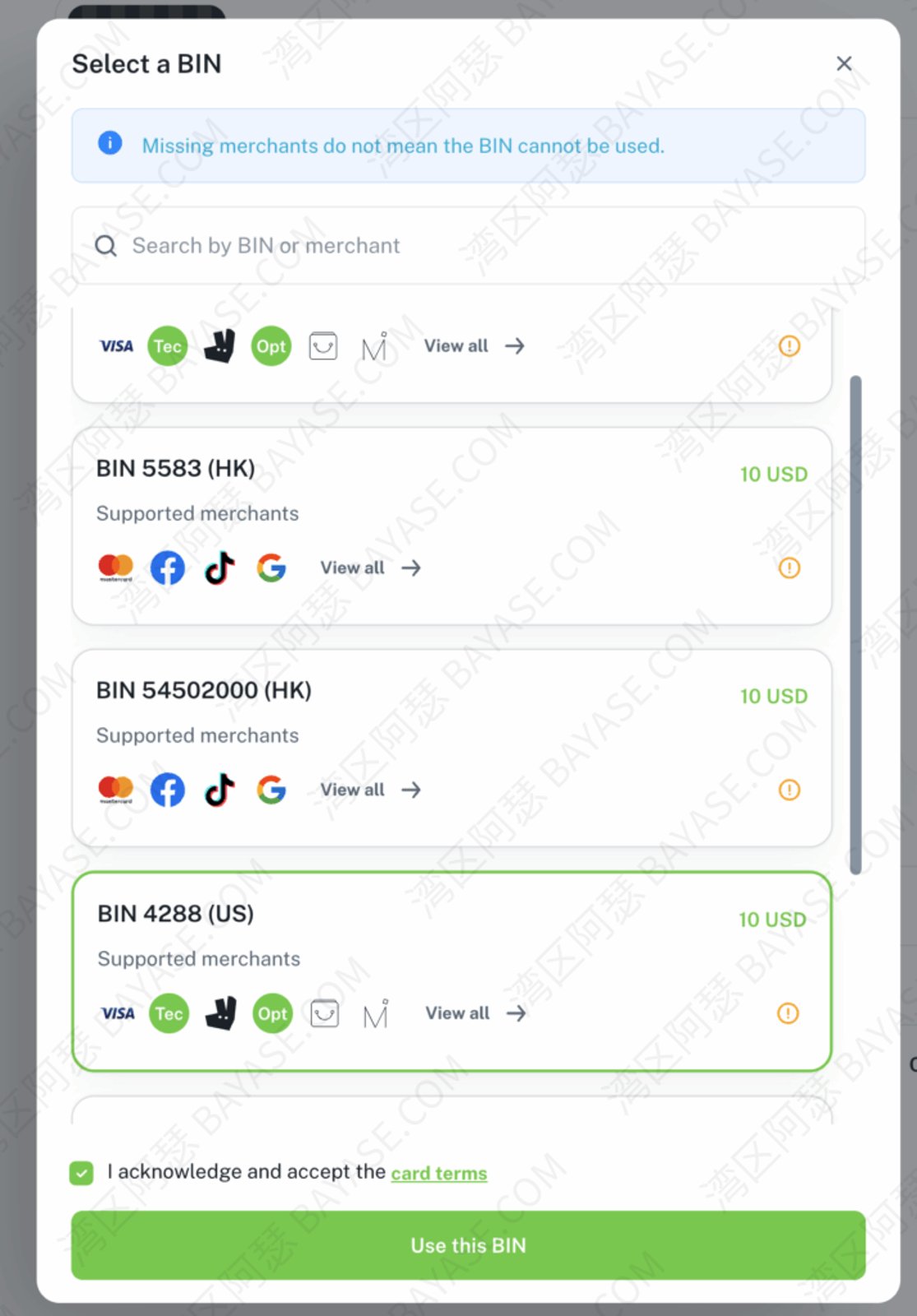

DogPay currently has three main BIN segments:

All three segments can be used for normal consumption and support the services listed in the table.

But the only key difference is:

Only the 5371 US segment supports binding to Apple Pay / Google Pay.

Regarding GPT subscriptions, I have personally tested the 5371 segment: the first month $0 offer can be opened normally without any issues. Therefore, if your primary use is ChatGPT, Claude, or other AI tool subscriptions, I recommend prioritizing the 5371 segment.

To avoid hidden fees, I've also organized DogPay's fee structure for your comparison.

For detailed explanations, you can refer to my instructions in this video.

If you mainly use it for ChatGPT top-ups, AI platform subscriptions, or e-wallet (ApplePay/GooglePay) payments, I strongly suggest registering for DogPay through the [link below] to directly get the currently best 5371 segment:

Regarding DogPay, Arthur has also written a detailed introductory article:

BinPay is different from other platforms. You cannot choose cards based on BIN segments; it focuses on comprehensive consumption and long-term cost considerations. Therefore, BinPay divides cards into Advanced and Diamond cards. Both levels currently only support virtual cards.

| – | BinPay Advanced (Virtual) | BinPay Diamond (Virtual) |

| Card Fee | 25 USD | 50 USD |

| Monthly Fee | 0.00 USD | 0.00 USD |

| Top-up Fee | 1.30% | 0.70% |

| Withdrawal Fee | 0.50% | 0.00% |

| Transaction Fee | 0.00% | 0.00% |

| Gateway Fee (<50USD) | 0.3 USD/trans | 0.3 USD/trans |

| Gateway Fee (>50USD) | Waived | Waived |

| Exclusive Discount | $5 card fee discount + $3 top-up voucher | $5 card fee discount + $3 top-up voucher |

Furthermore, while the initial card opening cost of BinPay seems high, Arthur fought for some benefits with the BinPay operations team:

A 5 USD card fee discount + a 3 USD top-up cash voucher.

This brings the final initial cost of the Advanced card down to 17 USD. Saving 8 USD is enough to buy a Starbucks coffee.

Another point is that BinPay's KYC currently does not require a face scan. Certification can be completed directly with a passport or ID number, which is quite comfortable.

If your use is mainly daily consumption without a specific field, I strongly suggest registering for BinPay through the [link below] to immediately get the $8 cost reduction:

Arthur also wrote a dedicated article introducing BinPay:

“BinPay Review 2025: The Most Reliable Virtual Card for ChatGPT and Global Payments“

CoinePay is a platform Arthur used more in the early days. However, because it lacks an official APP, it wasn't very convenient for me, so I used it less later on.

But the advantage of this platform is that it is really suitable for e-commerce scenarios. Many cross-border friends say it's very worry-free for advertising or overseas shopping, with many options. You can see the consumption ranking on the official website; spending is concentrated in these five scenarios, the second being Google Ads…

Looking at the differences in CoinePay card levels, it’s mainly a balance between the card fee and subsequent usage fees:

| Card Level | USA Standard | USA Platinum | USA Black Gold |

| Card Fee | 2.99 USDT | 6 USDT | 18 USDT |

| Monthly Fee | 1 USDT | 0.5 USDT | 0 USDT |

| Top-up Fee | 2.00% + 0.28 USD | 1.80% + 0.28 USD | 1.50% + 0.28 USD |

| Min. First Top-up | 10 USDT | 10 USDT | 10 USDT |

So for long-term use, spending more on the initial card fee can save you a lot on top-ups and monthly fees later. If it's just for short-term use, I recommend the Standard card.

In addition to virtual cards, CoinePay also supports physical cards and transfer cards. If you have other consumption scenarios, such as offline swiping or global transfers, you can use this.

If you mainly do e-commerce advertising, I strongly suggest registering for CoinePay through the [link below] to avoid many unnecessary risk control traps:

Detailed introduction article can be found here:

WASABI Card is a platform I haven't actually used yet. This is mainly because I see some pop-up prompts saying Mainland China is not within the service range, which might lead to KYC failure, so I haven't tried it.

However, the platform has some features. When opening a card, it specially marks the supported services and the services supported by each card BIN. Although DogPay has this too, DogPay doesn't have as many segments.

WASABI CARD is mainly divided into three card types:

If your usage scenarios are very diverse and you want to save trouble, I strongly suggest registering for WASABI Card through the [link below] to see if there is a virtual card suitable for you:

PokePay is a global multi-currency payment platform headquartered in Hong Kong. It is suitable for users needing cross-border payments and digital subscriptions. Especially for Mainland China users, it supports binding with Alipay for local payments.

In my experience, opening GPT with this card is a bit picky about the network environment; you might need a more native network to complete the payment.

If you don't need to open many virtual cards and want to get an overseas physical card at a low cost, I strongly suggest registering for PokePay via the [link below]. You can get one for 88 USD with free shipping in the Asia region:

Detailed content for friends can be found in this article:

The billing address is a commonly used identity verification factor in risk control, especially for Address Verification Service (AVS). The system compares your entered address with the issuer's record. If the format is non-standard or mismatched, it leads to failure.

The first six digits (BIN) influence risk control strategies. Some old or high-risk BINs might be blacklisted. Before opening, confirm the BIN is active for your target channel. Real virtual cards must have real BINs.

Maintain enough balance. Even a small pre-authorization might require a few dollars.

Arthur's one-minute decision guide based on latest 2026 data:

In 2026, owning a reliable virtual card is a “rigid demand” for overseas work and entertainment.

🎁 Reader Benefit: Leave a comment if you have issues, or refer to Arthur's “USDT Top-up Nanny-level Tutorial.“ Registering through links in this article may qualify for extra card fee cashbacks on some platforms!

A1: Generators are random numbers with no funds. Real platforms (DogPay, Roogoo) are issued by compliant institutions with real balances.

A2: Yes. Global compliance requires it. It improves security and reduces risk control blocks.

A3: Usually due to: 1. Blacklisted BIN; 2. Mismatched billing address and IP; 3. Insufficient balance. Use 5371 segments for higher success.

A4: Almost all: ChatGPT Plus, OpenAI API, Claude Pro, Midjourney, Netflix, Apple ID, Google Ads, TikTok Ads, Amazon, etc.

A5: Not if it's a regular card from a real platform. Bans usually come from “black market” credit cards or shady third-party top-ups.

A6: Most no longer support this. Use USDT. Check Arthur's Binance tutorial for details.

A7: Varies. DogPay usually has no monthly fee. Roogoo, on the other hand, offers different tiers, all with a 0 USD card issuance fee.

A8: Follow the “pay-as-you-go” principle. Don't keep large sums of money. We only recommend currently stable platforms.

That's the end — thanks for reading!

Here are some communities created by Arthur. Feel free to join if you're interested:

The Telegram groups have fewer chat restrictions. Just add the bot and select the type of community you'd like to join:

You can also add Arthur as a Telegram contact:

Connect with Arthur and stay closer.

Disclaimer: The content of this article reflects personal opinions only. Any financial actions taken based on this information are at your own risk, and any resulting losses shall be borne solely by the operator.